In 2018 the British Columbia government announced major changes to the Insurance (Vehicle) Act (“IVA”), with the intention of addressing a significant increase in the cost of claims over recent years. The most significant change comes in the form of a “minor injury cap”, which will provide an upper limit to non-pecuniary damages claimed for motor vehicle accidents in which only “minor injuries” were sustained. This applies to accidents occurring on and after April 1, 2019.

Although the main focus of attention has been on the minor injury cap, the legislation has also quietly made other significant changes, including an increase in accident (medical) benefits, an increase in wage benefits, and the expanded deductibility of certain benefits from tort awards, reducing tort damages in certain cases.

Part 1 of this two-part post explores how a minor injury is defined under the new legislation. Part 2 discusses how minor injuries are dealt with and also reviews changes to the no-fault accident benefits regime under the IVA, closing off with some key takeaway points.

The following are some key dates to keep in mind:

- January 1, 2018: statutory accident benefits (Part 7 benefits) increase to $300,000 from $150,000, retroactive for all accidents occurring on or after January 1, 2018.

- May 17, 2018: effective for accidents occurring on or after May 17, 2018, the categories of benefits deductible from tort awards are expanded. Courts will no longer take the likelihood of payment of benefits into consideration when deducting benefits paid or payable from tort awards.

- April 1, 2019: minor injury legislation applies to accidents occurring on or after this date, notably capping non-pecuniary damages for minor injury claims at $5,500. Section 82(2) limiting recovery for costs of health care treatments in tort claims also applies to accidents occurring on or after this date. Enhanced no fault benefits, including increased weekly wage loss payments (from $300/week to $740/week) and homemaking benefits (from $145/week to $280/week), also come into effect for accidents occurring on or after April 1, 2019.

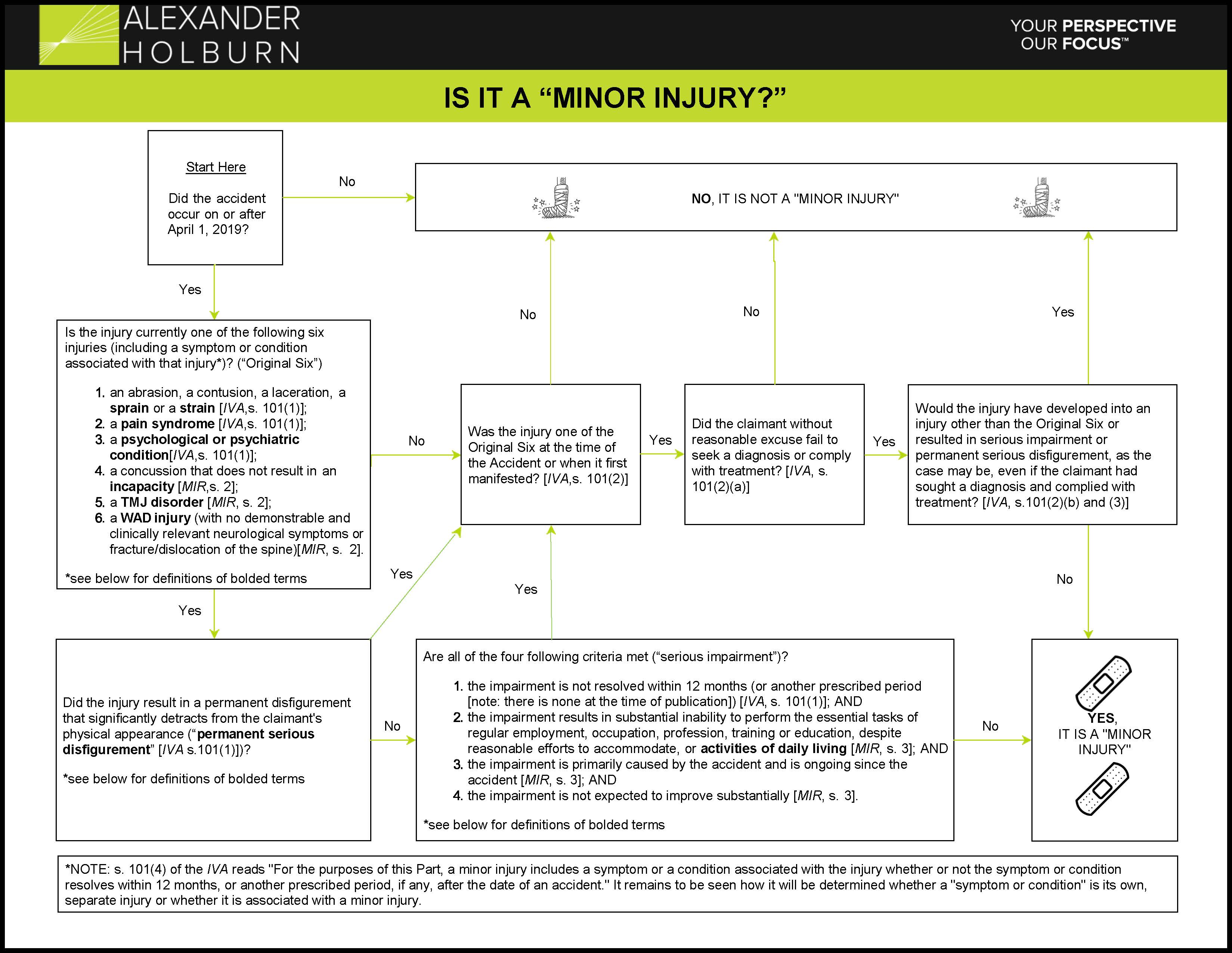

What is a Minor Injury?

“Part 7 – Minor Injuries” has been added to the IVA, effective for accidents occurring on or after April 1, 2019. Section 103 provides an upper limit (a “cap”) on the amount of damages recoverable for non-pecuniary loss arising from minor injuries suffered in a motor-vehicle accident to $5,500 (indexed to inflation). Non-pecuniary damages for claims involving non-minor injuries remain subject to cap set by the Supreme Court of Canada (presently at approximately $370,000).

The biggest question is how minor injuries are being defined. The government retains much latitude due to the fact the definition of minor injury is left to be expanded by regulation, specifically the Minor Injury Regulation (“MIR”), which was created on November 9, 2018, by way of an Order in Council. Accordingly, the government can continue to expand or refine the definition of minor injury without passing new legislation.

The result is a somewhat complicated process that involves referring back and forth between the IVA and the MIR to determine whether an injury is minor or not. Our associated flowchart “Is it a Minor Injury?” provides a helpful visual guide to making that determination.

The primary definition of “minor injury” is found in s. 101 of the IVA:

“minor injury” means a physical or mental injury, whether or not chronic, that

(a) subject to subsection (2), does not result in a serious impairment or a permanent serious disfigurement of the claimant, and

(b) is one of the following:

(i) an abrasion, a contusion, a laceration, a sprain or a strain;

(ii) a pain syndrome;

(iii) a psychological or psychiatric condition;

(iv) a prescribed injury or an injury in a prescribed type or class of injury;

Therefore, an injury is a minor injury if (1) it is one of the injuries defined in the IVA or prescribed in the MIR and (2) it does not result in serious impairment or permanent serious disfigurement.

i. Further Defined Minor Injuries

The MIR expands the definition of minor injury by prescribing additional injuries and types or classes of injuries that will be included in the definition of “minor injury”. The consolidated list of defined and prescribed injuries or classes of injuries falling under the designation of “minor injury” is as follows:

- an abrasion, a contusion, a laceration, a sprain or a strain [IVA, 101(1)];

- a pain syndrome [IVA, 101(1)];

- a psychological or psychiatric condition [IVA, 101(1)];

- a concussion that does not result in an incapacity [MIR, s. 2];

- a TMJ disorder [MIR, s. 2];

- a WAD injury (with no demonstrable and clinically relevant neurological symptoms or fracture/dislocation of the spine) [MIR, s. 2].

Complicating the definition more, all of the bolded terms in the above-referenced list are further defined in s. 1(1) of the MIR. See Appendix A for the legislative definition of these terms

ii. Serious Impairment or Permanent Serious Disfigurement

Even if an injury is one of the six listed above, it will not be considered to be a minor injury if it results in “serious impairment” or “permanent serious disfigurement”. However, there are a number of criteria that must be satisfied in order to fit within one of these two definitions.

It is easiest to first consider whether a minor injury caused a “permanent serious disfigurement”, defined in s. 101 of the IVA as “a permanent disfigurement that significantly detracts from the claimant’s physical appearance”.

If it is not a “permanent serious disfigurement”, the injury can still fall outside the minor injury category if it results in “serious impairment”. “Serious impairment” means a physical or mental impairment that meets all of the following four criteria:

- the impairment is not resolved within 12 months (or another prescribed period [note: there is none at the time of publication]) [IVA, s. 101(1)]; AND

- the impairment results in substantial inability to perform the essential tasks of regular employment, occupation, profession, training or education, despite reasonable efforts to accommodate, or activities of daily living [MIR, s. 3]; AND

- the impairment is primarily caused by the accident and is ongoing since the accident [MIR, s. 3]; AND

- the impairment is not expected to improve substantially [MIR, s. 3].

“Activities of daily living” is also further defined in s. 1(1) of the MIR (see Appendix A).

iii. Mitigation

Finally, even if the injury has been shown to result in serious impairment or permanent serious disfigurement, there is another test to pass before an injury will fall out of the definition of minor injury. The injury will still be considered a minor injury if the claimant failed to seek a diagnosis or failed to comply with treatment, unless the claimant can establish that the end result would have been the same even if a diagnosis had been sought or treatment complied with [IVA, s. 101(1) see definition of “serious impairment”]. In other words, if the injury started as a minor injury and would have remained a minor injury had a diagnosis or treatment been sought and followed, the injury will still be considered a minor injury even if it has, on its face, become more serious.

The result of this legislative puzzle is a broad definition of minor injury that is ripe for interpretative argument in the courts. It is likely that there will be significant argument over the meaning of the various terms (in particular the “substantial inability to perform the essential tasks…” part of the definition of “serious impairment”) used to define “minor injury”.

If you do not see the visual guide to understanding minor injuries below click here.

Now that you understand what a minor injury is, in Part 2 of this blog post we will discuss the new adjudication process for minor injuries in the Civil Resolution Tribunal (CRT) and the increase in no-fault benefits.